Market News

The Canterbury Construction Surge

What New Building Activity Means for Christchurch Property

As we delve into mid-2025, the Canterbury property market is showing fascinating shifts that every buyer and seller needs to understand. Recent building consent data reveals a complex picture of opportunity and challenge that could significantly impact your property decisions in the coming months.

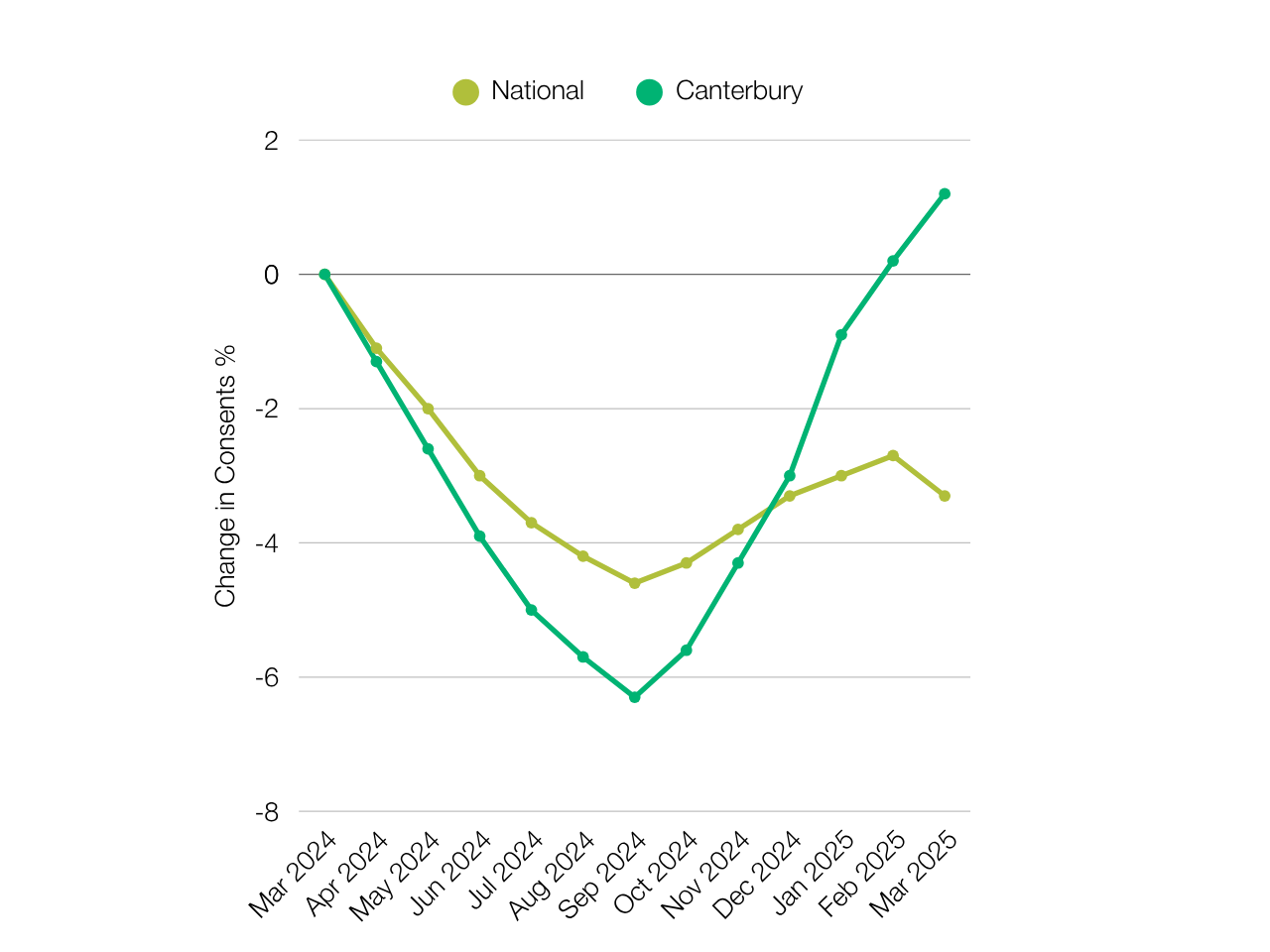

Canterbury Defies National Trends

While New Zealand's overall building consent numbers continue to decline, Canterbury is proving remarkably resilient. With 6,651 dwellings consented in the 12 months to March 2025, Canterbury accounts for 20% of residential construction across the country and has shown a slight improvement of 1.2%. This stands in stark contrast to other major regions, with Wellington Region down by 20% and Waikato down by 11%.

For Christchurch buyers, this resilience suggests continued competition for quality properties as new supply keeps pace with demand. However, it also indicates the market hasn't stalled like other centres, meaning prices are likely to remain stable rather than experiencing significant drops.

The Multi-Unit Development Factor

One of the most significant trends emerging in Christchurch is the shift towards multi-unit developments. Christchurch is showing growth on the back of high numbers of multi-unit developments, which the Canterbury Construction Report suggests might be a weak point over the next 6 to 12 months.

This trend has immediate implications for different buyer segments:

First-home buyers should pay attention to the increasing supply of townhouses and apartments coming to market. While this provides more entry-level options, the quality and long-term value of these developments will vary significantly.

Investors might find opportunities in well-located multi-unit developments, but should be cautious about over-supply in certain areas, particularly as the market expert warns of potential weakness in this segment.

Family home buyers may benefit from reduced competition as developers focus on higher-density housing, potentially creating better value in the established standalone home market.

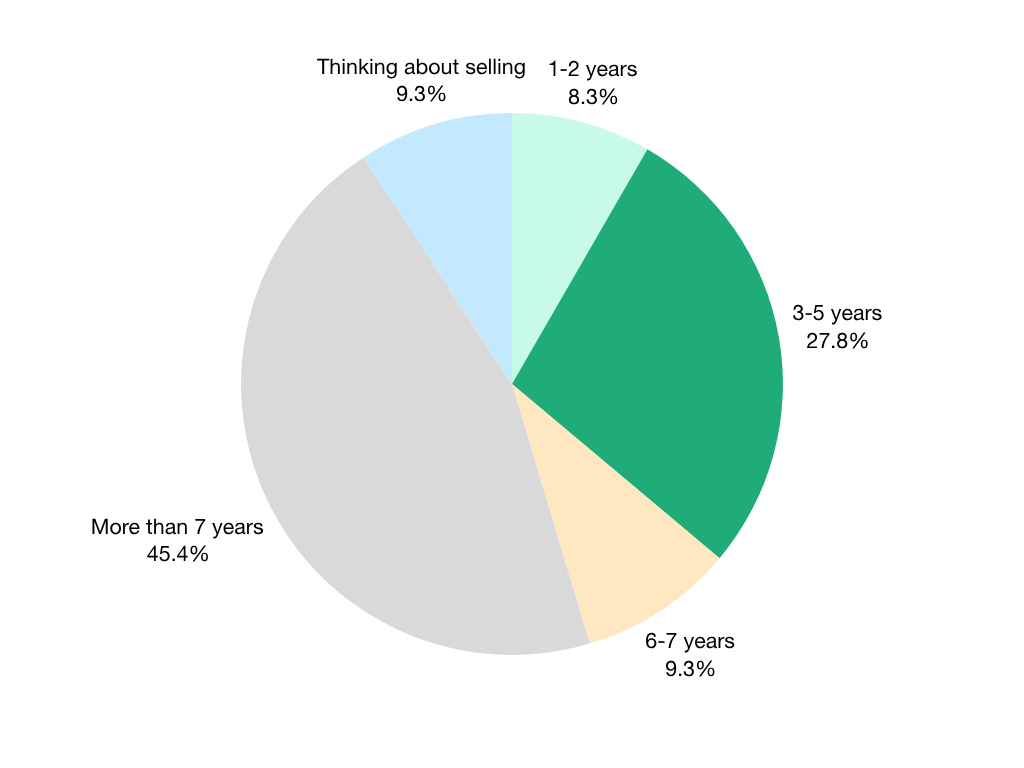

The Peak-Era Seller Wave

A particularly interesting insight from the data shows that 30% of homeowners planning to sell in the next 12 months have owned their homes for 3-5 years – these are properties purchased during the peak market of 2021-2022. This group represents a significant upcoming supply surge.

For sellers who bought at the peak: You may face challenging pricing decisions. These vendors will likely be anchoring to 2021 prices, so pricing strategy will be important. Working with agents who understand market psychology and can provide clear comparable sales data will be crucial.

For buyers: This creates opportunity. Motivated sellers who need to move for lifestyle or financial reasons may be more willing to negotiate, particularly if they've built equity through improvements or if their circumstances have changed.

The Buyer's Market Mindset

Canterbury buyers are showing remarkable confidence compared to national trends. 44% are looking to buy within the next 6 months and 29% within the next 12 months, both above national averages. This optimism is being translated into action, with buyers viewing 6-10 properties before making offers (down from 10-15 in March 2023) and completing purchases within 1-3 months.

This faster decision-making suggests buyers aren't waiting for significant price drops and are confident enough in current market conditions to act. For sellers, this means well-priced, well-presented properties are likely to sell within reasonable timeframes.

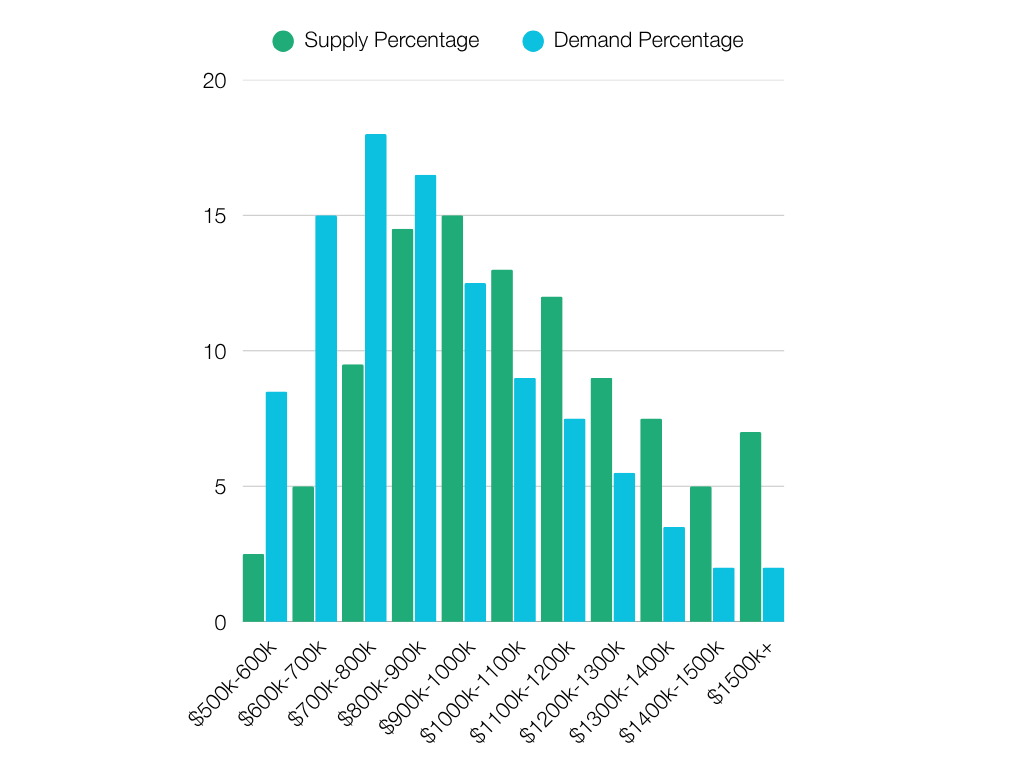

Supply and Demand Imbalance

One of the most critical factors affecting the Christchurch market is the supply shortage. A lack of suitable properties on the market is the biggest concern for Canterbury buyers, and Canterbury supply and demand data shows demand consistently outstripping supply across most price points.

The main concern for buyers is the lack of suitable properties on the market, so agents should focus on where demand is higher than supply. This suggests certain property types and locations will continue to see strong competition and price growth.

Market Timing and Momentum

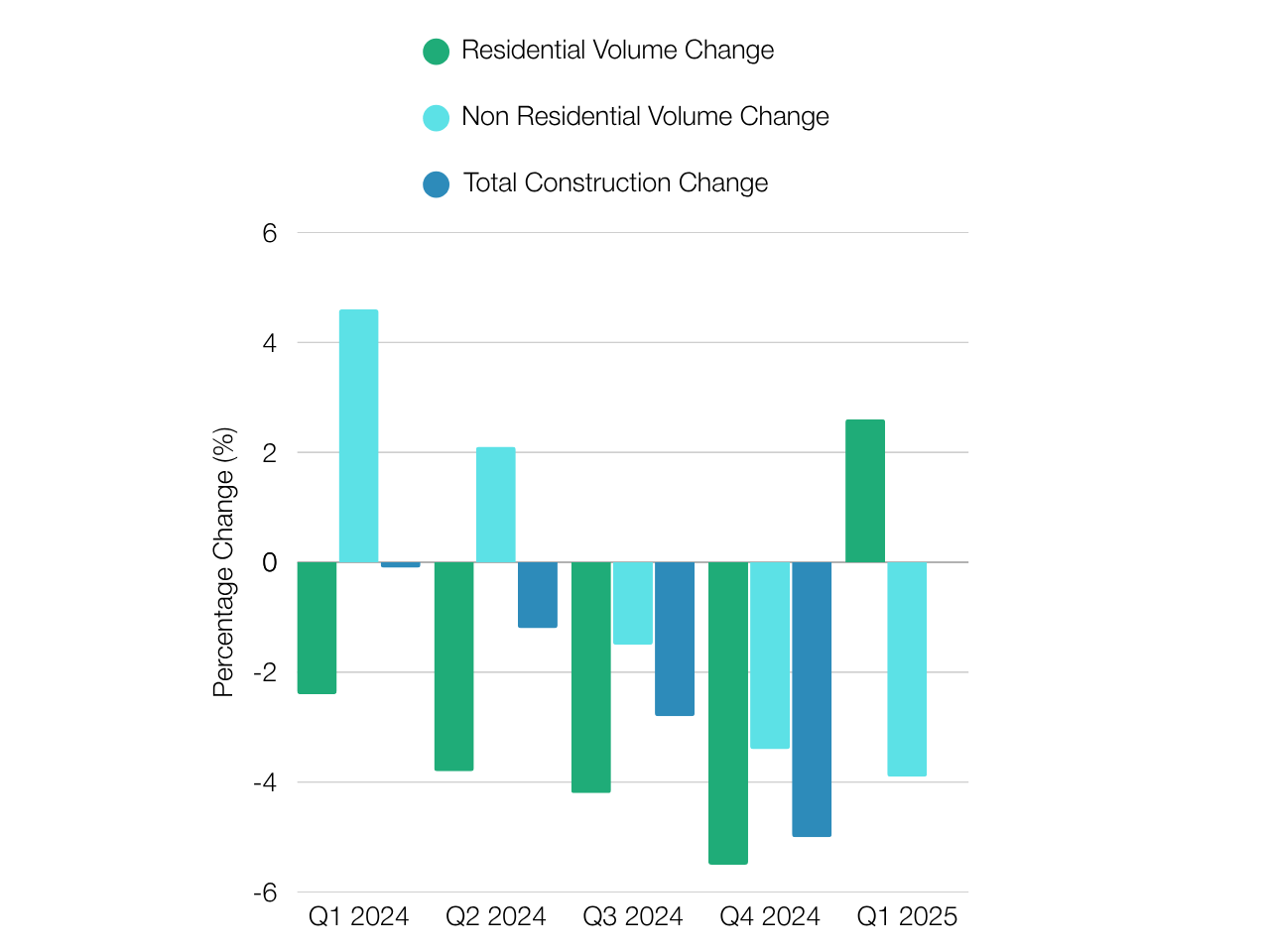

The broader construction data provides context for future supply. Nationally, new dwellings consented fell 16% in April 2025 after rising 11% in March, with 33,554 new dwellings consented in the year ended April 2025, down 5.2% from the previous year. Meanwhile, residential building volume rose 2.6% in the March 2025 quarter while non-residential fell 3.9%, though the actual value of building work was $7.6 billion, down 10% from the March 2024 quarter.

This suggests that while there's construction activity happening now, future supply will be constrained by the current slowdown in consents, potentially supporting price stability in the medium term.

What This Means for Your Property Strategy

If you're buying: Act decisively on properties that meet your criteria. The data suggests motivated buyers are succeeding, but indecision could mean missing opportunities in a supply-constrained market.

If you're selling: Timing matters. With peak-era owners entering the market and multi-unit developments adding supply, pricing will need to be realistic and competitive. The market is still functioning well for properly positioned properties.

For investors: Focus on location over development type. While multi-unit developments may face headwinds, well-located properties in areas with strong demand fundamentals should continue to perform.

The Canterbury market is showing resilience that sets it apart from other regions. With construction activity stabilising and buyer confidence remaining strong, the fundamentals point to a market that's finding its footing rather than falling into decline. For both buyers and sellers, understanding these trends will be key to making informed decisions in the months ahead.

1. Trade Me Property. (2025). State of the Nation 2025: Canterbury Property Market Report. Trade Me Property.

2. Blackburn Management Limited. (2025). New Zealand Construction Report: Residential Building Consent Index March 2025 Executive Summary. Canterbury Construction Report.

3. Statistics New Zealand. (2025). Building consents issued: April 2025. Retrieved from https://www.stats.govt.nz/information-releases/building-consents-issued-april-2025/

4. Statistics New Zealand. (2025). Value of building work put in place: March 2025 quarter. Retrieved from https://www.stats.govt.nz/information-releases/value-of-building-work-put-in-place-march-2025-quarter/

5. Statistics New Zealand. (2025). Building consents issued: March 2025. Retrieved from https://www.stats.govt.nz/information-releases/building-consents-issued-march-2025/

Other Posts By Jeremy

Property Report - August 25

Strong August sales confirm demand is alive in Christchurch. Get the complete breakdown in my latest market wrap.

Property Report - July 25

If you’ve been wondering how the Christchurch market is tracking through the middle of winter, here’s the wrap: it’s steady, resilient, and showing real depth.

We would love to hear from you

0800 673 769

Follow

Connect with Kelleher to hear about the latest resources and news